Optimizing Tax Lot Selling

Many clients have spent decades building a brokerage account by consistently saving, reinvesting dividends, and staying invested through the bumps. Now that they are approaching retirement, they are ready to start drawing it down. The question most people never think to ask until they are actually selling is which shares do you sell first? The answer to that question can save you thousands of dollars in taxes each year.

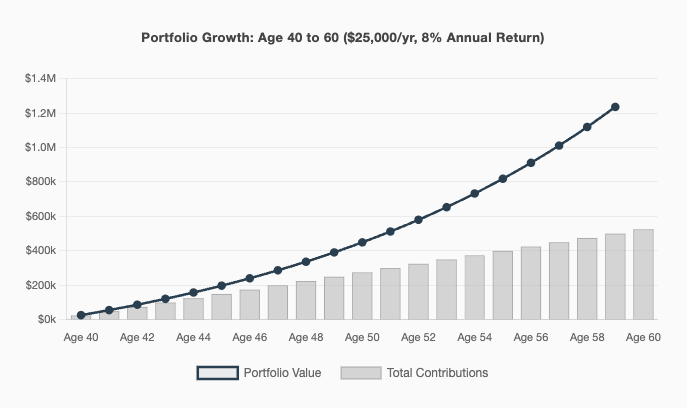

For example, John started investing $25,000/yr at age 40 in a global stock fund. By the time he is 60, it has grown to over $1.2mm, assuming 8% growth (not guaranteed).

At 60, John decides to start drawing down the account at 5% per year. With a $1,235,573 portfolio, that is about $60,000 annually. The fund keeps compounding at 8% (6% capital appreciation + 2% dividend reinvestment), so the balance continues to grow even as Jordan withdraws.

His brokerage account is not one lump of money. It is a collection of individual lots, each purchased at a different time and a different price. John's account contains two types:

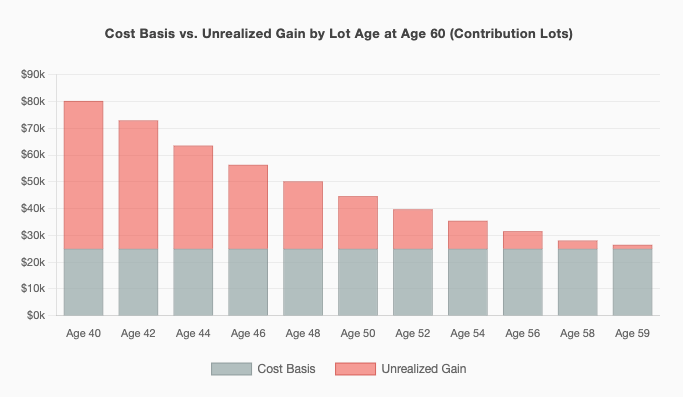

Contribution lots. Each year, John invested $25,000, which was treated as a separate lot with a $25,000 cost basis. The first lot, from age 40, has now grown at 6% per year for 20 years. The last lot, from age 59, has only had one year to grow.

Dividend reinvestment lots. Each year, the fund paid a 2% dividend, which he reinvested. Each reinvestment created a brand-new lot at whatever the share price was that day. After 20 years of this, the account holds dozens of small dividend lots, the most recent of which was purchased just months ago at today's prices.

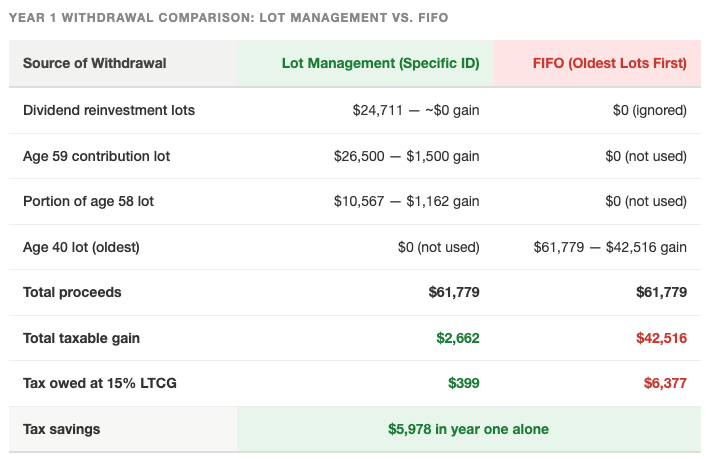

In the first year of withdrawal, John needs to pull out $61,779. The fund is already generating a 2% dividend reinvestment of $24,711. Those freshly reinvested dividend shares were purchased at today's prices. Their cost basis equals their current value. If John sells them immediately, the taxable gain is essentially zero.

So right away, John can cover $24,711 of the $61,779 withdrawal with near-zero tax cost. That leaves only $37,067 to source from older lots. And for that portion, John gets to choose which lots to sell. Using specific identification (the IRS method that lets you designate exactly which shares you are selling), Jordan sells the most recently purchased contribution lots first: the age-59 lot ($26,500, with only $1,500 in gain) and a portion of the age-58 lot ($10,567 worth, with about $1,162 in gain).

Total taxable gain on the full $61,779 withdrawal: $2,662.

Now compare that to what happens if John’s brokerage defaults to FIFO, first-in, first-out, and sells the oldest lot first. That age-40 lot is worth $80,178 on a $25,000 basis. Selling $61,779 worth of it means realizing a gain of about $42,500.

Assuming he continues with this strategy, he will likely pay significantly less in taxes over his retirement than if he chose any other lot option. And if he continues at this rate, there will be a significant amount of money left to his estate at his death, at which point they can get a full step-up in basis. The taxes aren’t deferred; they are completely avoided.

A few considerations -

Lots need to be long-term to get the preferential rate. Shares held less than one year are taxed at ordinary income rates. The dividend reinvestment lots from this year technically qualify for long-term treatment only after 12 months, so the timing of your sale matters. In practice, we will sell the prior year's dividend lots that have aged beyond 12 months and still carry a very recent basis.

This interacts with everything else on your return. If you are also collecting Social Security or taking Roth conversions, capital gains from lot sales can push other income into higher brackets or affect Medicare premiums. The lot-by-lot math does not live in isolation. A small amount of gain realized now can sometimes be better than a larger amount later, depending on your full income picture that year.

If you have a taxable brokerage account and are starting to draw it down, the default setting at your custodian is likely not the most tax-efficient option. Take some time to understand your lot structure and how to elect specific lots for sale.

Happy Planning,

Alex

This blog post is not advice. Please read disclaimers.