When Tax Brackets Lie to You

On paper, a retiree can look like they are firmly in the 12% bracket. In practice, their next dollar of income can cost nearly three times that. The reason is due to the way the tax system works, particularly something called “income stacking.”

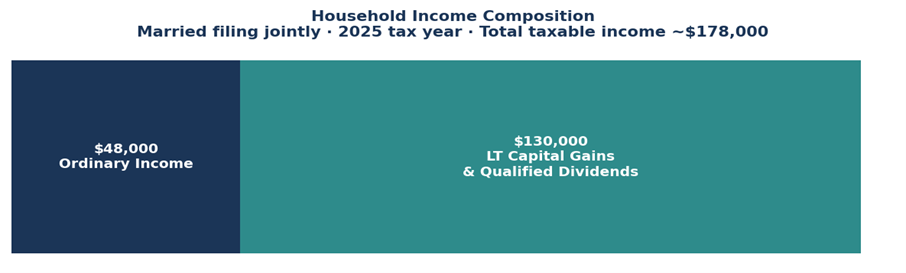

Take a retired couple, the Smiths. Their income this year looks like this: $48,000 in ordinary income from Social Security, a small pension, and interest, alongside $130,000 in long-term capital gains and qualified dividends from their brokerage account.

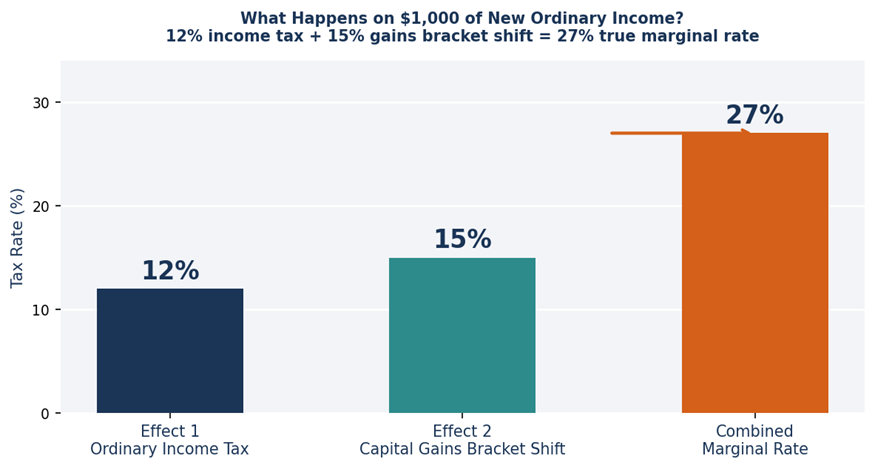

While their total income is $178,000, their tax rate on ordinary income is well within the 12% bracket, which extends to $100,800 for a couple filing jointly in 2026. So if they were to earn an extra $1,000 in income from a job, a Roth conversion, or something else, it should cost them $120 (12%), right? Not even close. Their real rate is closer to 27% on that next $1,000 of income.

Long-term capital gains and qualified dividends sit on top of ordinary income when the IRS calculates your tax. And those gains and dividends are taxed on a completely different scale than your ordinary income, with some income taxed at 0%, then 15%, then 20+%. When ordinary income is low, a big chunk of those gains falls in the 0% long-term capital gains bracket. But when you add a new dollar of ordinary income, two things happen at the same time:

1) that ordinary income gets taxed at your federal bracket rate (12% for the Smiths)

2) that same dollar pushes an equal dollar of long-term capital gains out of the 0% bracket and into the 15% bracket.

On $1,000 of new ordinary income for the Smiths, they pay $120 in regular income tax, plus $150 from gains pushed into the 15% bracket, equaling $270 total, a 27% marginal rate on income the bracket table said would cost 12%.

That gap exists for as long as your capital gains straddle the 0%/15% long-term capital gains threshold. For married filers in 2025, the threshold is $100,800 in taxable income.

The stacking problem tends to show up around events that look routine on the surface: a Roth conversion in early retirement, a part-time consulting project, required minimum distributions starting at age 73, or even reinvested dividends quietly pushing capital gains higher. Any of these can trigger the double tax hit.

So before you take a taxable distribution, do a Roth conversion, or make any move that adds ordinary income, find out where your long-term gains sit relative to the 0%/15% threshold.

Happy Planning,

Alex

This blog post is not advice. Please read disclaimers.