The Age 60-63 “Super Catch-Up”

Last year, as part of Secure 2.0, the “super catch-up” became available to pre-retirees saving in their 401k. It’s a generous rule, specifically for the four-year window between ages 60 and 63, that allows a meaningfully larger contribution during what are often peak earning years.

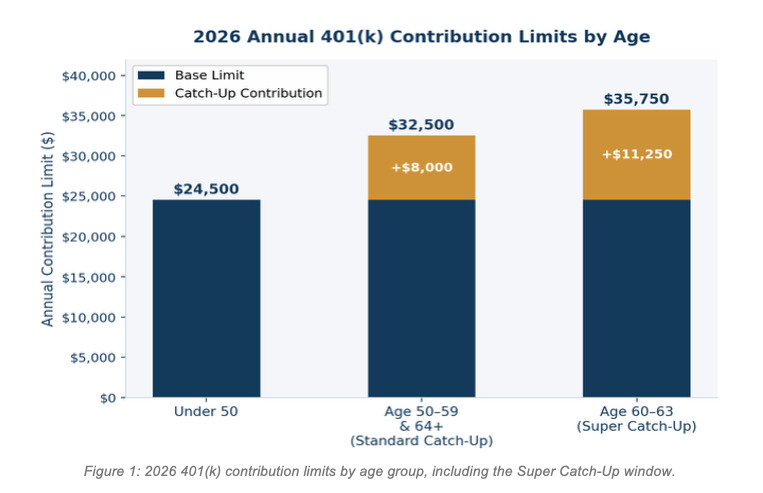

The IRS sets an annual limit on how much you can contribute to a 401(k). For 2026, that base limit is $24,500. But once you turn 50, you become eligible to contribute an additional “catch-up” amount on top of that. The standard catch-up limit for 2026 is $8,000, bringing the total to $32,500 for most workers 50 and older.

The Super Catch-Up replaces that standard catch-up amount for workers who are specifically ages 60, 61, 62, or 63 during the plan year. Instead of $8,000, those workers can contribute up to $11,250, an extra $3,250 per year compared to everyone else.

The eligibility window is precise. You must be age 60, 61, 62, or 63 during the calendar year of the contribution. The window begins the year you turn 60 and ends the year you turn 63. Strangely, when you hit 64, you revert back to the standard $8,000 catch-up.

It’s also worth noting that this rule applies to employer-sponsored workplace plans like 401(k), 403(b), and 457(b) plans. It does not apply to IRAs, which have separate and lower contribution limits.

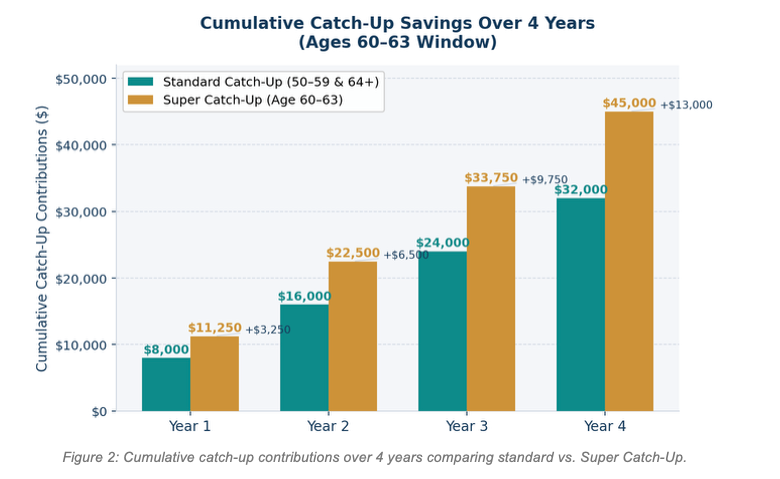

The window is short, but four years of maximizing contributions add up. Compared to someone using only the standard catch-up contribution, a person who maxes out each year from 60 to 63 will contribute an extra $13,000 to their retirement account over that period, before any investment growth.

The Super Catch-Up is one of those rare planning opportunities where the government is actively giving you a bigger shovel to dig your retirement savings. The window is short and specific. If you’re approaching 60, or already in that window, it’s worth a conversation to make sure you’re taking full advantage of it.

Happy Planning,

Alex

This blog post is not advice. Please read disclaimers.