When Pre-tax (not Roth) 401k Contributions Can Make Sense

Most people think of the Roth vs. pre-tax 401(k) decision as a simple bet on future tax rates. But there is a more specific opportunity hiding in that choice, particularly in the years leading up to retirement, and it has everything to do with where in the bracket structure your deduction lands versus where your Roth conversion starts.

The Deduction Comes Off the Top

Income tax is progressive. Each layer of your income is taxed at a different rate as it climbs through the bracket structure. Pre-tax 401(k) contributions shrink your income from the top of that structure. The lowest brackets stay exactly where they are.

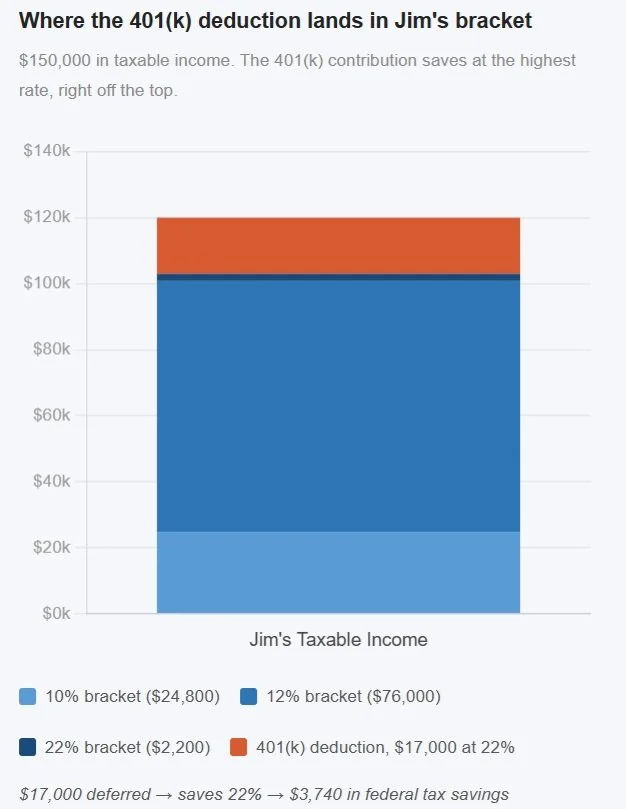

Take Jim, for example. His taxable income is $150,000 a year, which puts him solidly in the 22% federal tax bracket. When Jim contributes $17,000 to his pre-tax 401(k), that deduction does not get averaged across all of his income. It comes off the top. Every dollar of that $17,000 is reducing income that was being taxed at 22%, saving him exactly $3,740 in federal taxes. Jim's deduction hits his highest rate, dollar-for-dollar.

The 401(k) contribution peels right off the top of Jim's 22% bracket, and it is as clean a dollar-for-dollar exchange as you will find in the tax code.

The Flip in Retirement

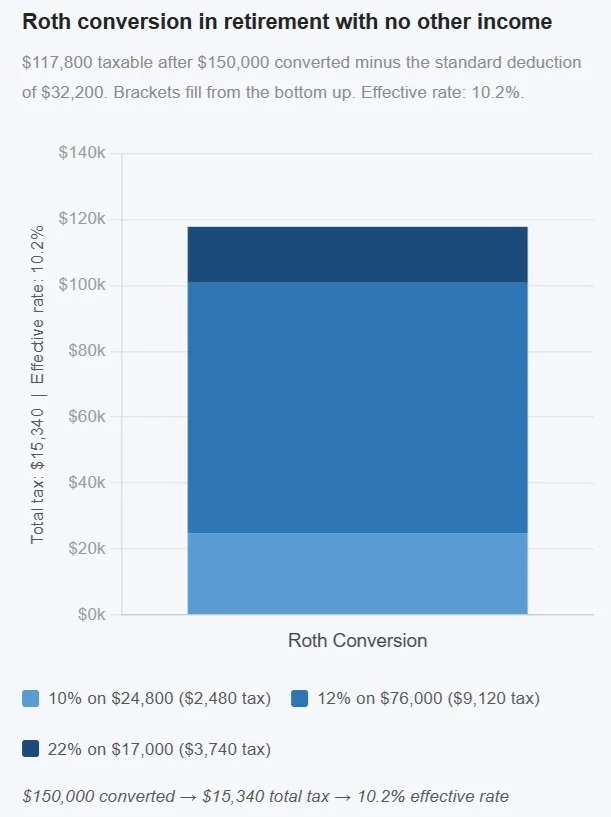

Now fast forward. Jim retires before Social Security starts. He has no wages, no pension, no significant income sources. He is living off cash savings. His taxable income is close to zero. He starts converting his traditional IRA.

When Jim converts $150,000 with no other income, not all of that amount is taxed at 22%. It starts from the bottom of the bracket structure and works its way up. The first $32,200 is tax-free (via the standard deduction). The next $24,800 is taxed at 10%. The next $76,000 is taxed at 12%. Only the final $17,000 reaches the 22% bracket at all.

That is an effective tax rate of about 10% on $150,000 of Roth conversion. Jim got a 22% deduction going in, and he pays a 10% effective rate coming out, a gap of 12%.

The Window Closes

This only works if Jim actually has low-income years in early retirement. Once Social Security starts, those lower brackets fill up quickly. Once required minimum distributions begin at age 73, they can push taxable income well into the 22% bracket or higher, shrinking or eliminating the spread entirely.

The planning work is identifying those years between retirement and when income sources kick back in, and figuring out how much to convert each year. Convert too little, and you leave the opportunity behind. Convert too much in one year, and you push yourself into a higher bracket unnecessarily.

Happy Planning,

Alex

This blog post is not advice. Please read disclaimers.