The Future of Social Security (2026 edition)

One of the most common questions I get on the topic of Social Security in a new client's retirement plan is "Will there be anything left when I retire?" It's a fair question given the solvency issues of the Social Security trust fund.

Like most issues, the media loves to discuss the problem and rarely the solution.

Fortunately, there is data to answer these questions. Every year, the Board of Trustees for Social Security reviews the financial status of the trust fund that pays out Social Security benefits. Recently, the board released its 2026 report, and below is my summary.

Summary of 2026 Report

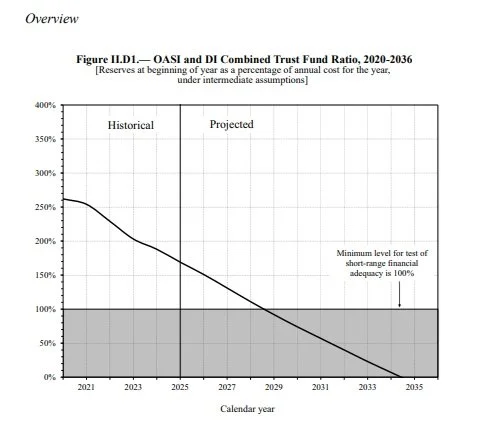

Current Costs and Income - In 2025, total program income was about $1.45 trillion, while total program cost was $1.61 trillion. That means Social Security ran a deficit of roughly $160 billion for the year, drawing down its reserves to cover the gap. At the end of 2025, total reserves stood at $2.56 trillion, down from $2.72 trillion at the start of the year.

From 2026 to 2034 – The reserves are currently $2.56 trillion. Total costs are projected to be more than income every year until the reserves are depleted. In 2034, they are projected to be depleted, matching last year’s report.

This is the part that worries people, so I want to be direct about what depletion actually means. It does not mean Social Security goes away. It means the program would only be able to pay out what it collects in payroll taxes each year. At the point of depletion in 2034, the program could cover about 83% of scheduled benefits. That percentage would decline gradually to around 65% by 2100 if nothing changes. However, there are several possible solutions to prevent this that I believe politicians will make, unfortunately, probably later rather than sooner.

Solutions – The board provided many different solutions, three of which have been widely discussed.

Increase payroll taxes by 12.4% to 16.65%. This could mean both the employee and employer pay an additional 2.1% into Social Security.

Increase the retirement age for younger workers (i.e, can’t claim benefits until 70 or later).

Cut benefits by 25.2%.

I think it’s likely that it won’t be an all-or-nothing solution. There may be a slight increase in taxes and the retirement age. There may be a slight cut to benefits. I do not want these solutions to downplay the seriousness of the issue. Action should be taken, preferably sooner rather than later, to protect current and future generations. But there are reasonable steps that can be taken to keep Social Security in place for many years to come.

Happy Planning,

Alex

This blog post is not advice. Please read disclaimers.